What Is KYC Remediation? Definition, Process and Compliance

It’s no fun to realize that most of your customer profiles are outdated, incomplete, or worse – non-compliant, especially when you know that Anti-Money Laundering (AML) regulators are watching and penalties for non-compliance reach into the millions. That’s exactly the headache that KYC remediation can cure, or rather “remedy”.

Know Your Customer (KYC) remediation is the systematic process of reviewing, updating, and correcting existing customer information to meet current regulatory standards. Whether you’re dealing with legacy records from years ago or adapting to new compliance requirements, understanding KYC remediation is essential for protecting your business from regulatory action and maintaining customer trust.

What is Remediation in Banking?

Since banks are under constant and very strict regulatory pressure, they take KYC remediation particularly seriously. Not to mention the threat of massive financial penalties for AML failures that banks face. The non-compliance fines for banks are huge, putting their licenses to operate at risk.

KYC remediation in banking basically means fixing outdated, inaccurate or incomplete customer data – all with the aim to meet regulatory standards. Remediation involves a thorough review to ensure customer profiles reflect accurate identity, risk status, and compliance the anti-money laundering and counter-terrorism financing (CFT) obligations.

Research shows that inaccurate, outdated, and incomplete customer data is a primary driver for remediation projects. And when it comes to poor data, KYC remediation means cleaning or improving the quality of data by:

- Identifying inaccuracies

- Noticing missing information

- Obtaining the missing information

- Removing redundant or irrelevant data

After such a clean-up, data is reliable and compliant.

The core purpose of KYC remediation in banking is to guarantee that all customer records and processes comply with constantly changing laws, including AML, data protection (like GDPR), and tax reporting. All this is done in order to get to a state where all data is regulator-proof.

To achieve such “clean” status, the KYC remediation process targets the legacy customer files whose information has grown outdated over time, because bringing older records up to current legal standards is key for banks. And it shouldn’t be a reactive but rather a proactive (preventative) measure.

But how should this be done? For banks, it’s very important not to remedy customer information haphazardly. There should be a structured, comprehensive, and systematic approach to ensure that all outdated accounts are reviewed, this way creating a clear audit trail.

As you can see, KYC remediation in banking means correcting the past to protect the future. Key goals are to avoid penalties and to improve risk management, customer service, and security.

The global KYC remediation services market size was $2.84 billion in 2024 and is projected to grow to $8.13 billion by 2033. Source

Why KYC Remediation Matters

Although KYC remediation may sound like a headache, it’s importance (for financial institutions especially) can hardly be overestimated. Let’s underscore the key reasons the KYC remediation process is critical:

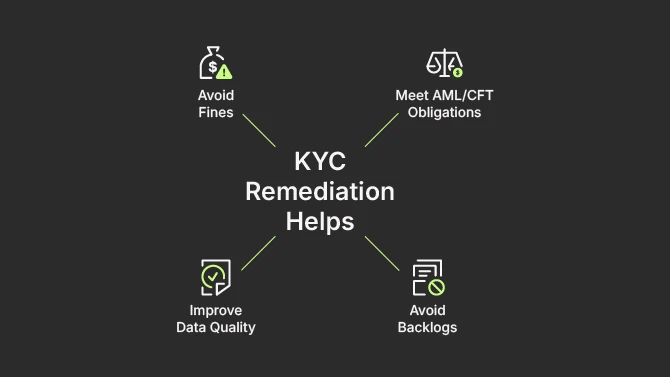

Avoiding costly fines. Regulators worldwide are cracking down on AML/KYC lapses with unprecedented intensity. Inadequate customer due diligence (CDD) and ongoing transaction monitoring failures remain the most frequent and costly failures cited by regulators like the OCC and the FinCEN.

The largest single penalty in 2024, and a clear indicator of regulatory severity, was $3.1 Billion imposed to TD Bank by multiple US authorities (DOJ and FinCEN). The reason is that TD Bank allowed over $670 million in criminal proceeds (including drug money) to be laundered through its system due to systemic failures to maintain an adequate AML program and file timely Suspicious Activity Reports.

Improving data quality. Obsolete or incorrect customer data poses a serious business risk, as it becomes harder to detect money laundering or fraud. If you’re trying to assess a client’s risk when their profile lacks key details or hasn’t been updated in 5 years – their risk rating could be way off.

Meeting AML/CFT obligations. Compliance laws and regulations change frequently, and each change can render yesterday’s compliant records incomplete today. That’s why KYC remediation is the mechanism that helps organizations keep up with the ever-changing regulations, especially AML/CFT obligations.

Avoiding disruptive backlogs. Neglecting KYC reviews can result in a massive backlog of poor data that’s both expensive and disruptive to clear. To put this into perspective, 40% of banks report that a single corporate KYC review takes 30–60 days, and some banks take up to 150–210 days for just one review. That’s an enormous operational burden. That’s why remediation done in a timely, systematic way helps organizations avoid rushing to update thousands of files under regulatory pressure.

Failing to remediate KYC risks exposes banks to regulatory sanctions, financial loss, and reputational damage.

When to Initiate the KYC Remediation Process

Commonly, there are certain triggers that signal it’s time to start the KYC remediation process and clean up customer records. Let’s review six key scenarios:

- Changes in regulations. Probably the most frequent trigger is a change in laws or the introduction of new KYC requirements. When authorities update AML rules or introduce standards for identifying ultimate beneficial owners (UBOs) or politically exposed persons (PEPs), existing customer files must be updated to comply.

EXAMPLE: The US INFORM Consumers Act of 2023 required online marketplaces to verify certain seller information (like bank account and tax ID). Many marketplaces had to launch remediation campaigns to gather that data from all sellers meeting the criteria. - Audit findings. Failed regulatory KYC audits or inspections often mandate remediation. When regulators identify deficiencies, such as incomplete files or missing documents, organizations must launch projects to correct those gaps. To be more precise, KYC remediation is often a direct response to enforcement actions or audit failures.

- Periodic reviews. Banks review customers on risk-based schedules: high-risk annually, medium-risk every 2 years, low-risk every 3-5 years. These scheduled, proactive risk-based refreshes ensure information stays current and compliant.

Note: Note: some differentiate “KYC refresh” from “KYC remediation”: refresh is routine, whereas remediation is a larger one-off fix, but fundamentally both involve updating KYC data. - Data quality issues. Internal problems may also trigger remediation. IT system migrations, mergers, or acquisitions may reveal missing information, identify outdated data, find errors, or inconsistent KYC standards across customer records that need fixing.

- Major events. Significant changes that affect many customers always require targeted updates. Examples include new sanctions, expired IDs across many accounts, or upgraded systems detecting previously unidentified PEPs. Basically, any event that suggests current records are out-of-date or insufficient should set a remediation effort in motion.

- Dormant accounts. Long periods of customer inactivity signal that the information you store is outdated. Best idea is to start with accounts with no transactions or updates for years, as these may need not only review or updating, but even closure to reduce risk. An account that hasn’t been touched in years might indicate the person is no longer alive or using the bank.

To complicate things even further, many of these triggers can overlap or happen together. That’s why you should not wait for a critical situation to occur. Instead, you should treat KYC remediation as an ongoing necessity – a critical part of the regulatory compliance lifecycle.

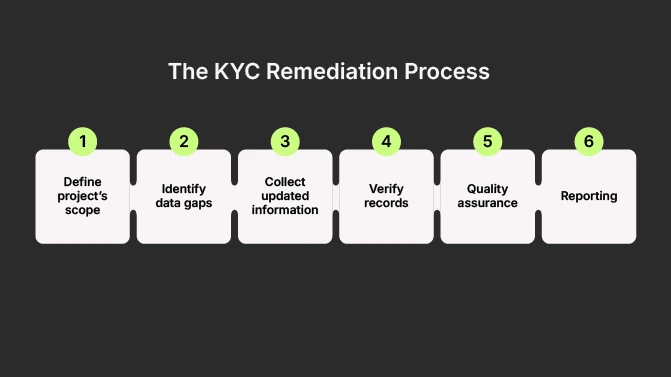

The KYC Remediation Process Step-by-Step

To make KYC remediation less complicated an endeavor, it’s best to break it into clear steps, which will help manage the process effectively. Let’s dissect a typical and successful KYC remediation process.

STEP 1. Define the project’s scope

Start by determining which customers or accounts need remediation and what data gaps must be addressed. For example, if a new regulation is the cause of remediation, you need to identify all customers who lack the newly required data field. If it’s a periodic refresh, then you need to decide which segment (high-risk clients, or those not reviewed in 3+ years, etc.) are in scope. It’s crucial to prioritize here: many banks choose to remediate in phases, tackling highest-risk or most non-compliant files first. Define your remediations scope, set objectives and timelines, and assign responsible people.

STEP 2. Identify data gaps

This step is about pinpointing what exactly needs fixing. Assess existing customer databases to find incomplete, outdated, or suspicious records. Usually this could be automated, so you don’t waste time manually looking for data gaps. Once you have your checklist of remediation tasks, you can move on to the next step.

STEP 3. Collect updated information

Often the most labor-intensive, this step requires you to contact affected customers and request missing documents or information. Clearly explain what’s needed, why it’s necessary, how to submit it, and any deadlines or consequences for non-compliance. For example, a common KYC remediation scenario is reaching out to a customer whose ID on file has expired. So, you would request a renewed ID document to meet updated identity verification requirements. Also, make sure it’s easy for your customers to respond.

STEP 4. Verify and update records

At this point, your KYC specialists (or outsourced automated systems) need to verify the authenticity and completeness of the new customer information. So, if a customer provides a new passport scan, it needs to be verified (either via an automated document check or via a manual review) to ensure it’s legitimate and belongs to the customer. You also need to screen updated data against sanctions and PEP lists, then add verified information to customer profiles while removing obsolete data.

STEP 5. Quality assurance

Now it’s time to audit the remediated files to ensure everything is of good quality. At this stage you will be looking for errors: do all new documents have legible images, or maybe something was automatically checked and verified, although it wasn’t. Also, it’s advisable to maintain detailed AML audit trails, documenting all actions, changes, and reviewers for regulatory compliance. This way you can demonstrate to regulators that you took all necessary KYC remediation steps. In the end, you should have a report or certification proving that X number of accounts were remediated, with evidence to show for each.

STEP 6. Reporting

Finally, you need to summarize your remediation outcomes, including all accounts updated and issues discovered. If during remediation you found any new suspicious information, proper reporting to authorities, such as filing suspicious activity reports, should be done immediately as required by law. Use all the learnings and findings to improve your ongoing KYC processes and prevent future gaps. For example, if the remediation project revealed a certain pattern of data becoming outdated, you may want to adjust your ongoing KYC review frequency or invest in a better KYC technology.

KYC Remediation Challenges and How to Solve Them

KYC remediation comes with several challenges – from data overload to customer pushback. But if you’re aware of them, there are ways to overcome them.

The first challenge is the sheer volume of new data and the complexity of the data remediation process. Typically, large financial institutions, such as banks, may have millions of records to update. And each customer profile can contain numerous data points, and required documents vary by customer type and jurisdiction, adding complexity. Solution: Use a risk-based approach to prioritize high-risk accounts first. Then, automate gap identification with data analytics and consider outsourcing for large-scale campaigns.

Second, it may be difficult to balance speed and accuracy due to regulatory deadlines. Being under pressure, you try to work quickly, but rushing causes errors, which defeats the purpose by causing compliance failures even after remediation. Solution: Create a clear workflow and realistic timelines with quality checkpoints. Use automation to eliminate human error in repetitive tasks. For instance, use OCR (Optical Character Recognition) to extract data from IDs rather than typing it, or use validation scripts to flag inconsistent entries.

Third, KYC remediation requires a lot of resources: both people and money. Often requires a dedicated team of analysts working for months, plus significant IT support and training. No surprise that many organizations find it challenging to allocate sufficient skilled AML/KYC compliance staff. Solution: Use AI-driven platforms to automate data collection and verification to cut labor costs substantially. Foster cross-functional collaboration – involve IT, operations, and front-office staff in the effort so that the compliance team isn’t isolated and the workload is spread out.

Big banks in certain EU countries spend an average of €5.7 million annually on KYC, with 74% of that on labor – while automating KYC processes can cut these costs by over half. Source

Here comes one of the trickiest challenges – managing customer experience during remediation. Customers may be confused or annoyed by requests to resubmit information. Requests may appear as inconvenient or even suspicious to the customer, so you may risk damaging trust or losing business even. Solution: Always communicate transparently about why updates are needed and how they benefit customers. Provide easy submission channels and train service teams to handle concerns empathetically. Do not spam customers with constant reminders, but do follow up judiciously before resorting to account restrictions.

Another headache is to keep up with regulatory uncertainty. Rules can change mid-remediation, creating a moving target, meaning what’s compliant today might shift if a new rule comes out tomorrow. Solution: Continuously monitor regulatory changes and build flexible processes that can adapt quickly to new requirements. This means your compliance team (or a RegTech tool) should track upcoming laws or guidance and adjust internal policies promptly.

Finally, legacy systems can create data silos and new technology integration challenges, when updated information doesn’t properly sync across departments. Solution: Choose solutions that are compatible with your existing IT infrastructure; many modern KYC platforms offer APIs and modular integration that can overlay legacy cores. Also, you may want to invest in a unified customer lifecycle management system that centralizes KYC data And, don’t forget to test integrations on small data sets first, and ensure all departments align on tools and data flows.

Using Technology to Streamline KYC Remediation

Spreadsheets, phone calls, copying documents, and other traditional KYC methods simply can’t scale to meet modern compliance demands. Luckily, today’s RegTech and FinTech solutions offer powerful alternatives that help organizations, especially financial institutions, automate and streamline remediation tasks. Let’s take a closer look at how technology can make a difference:

Efficiency and Cost Savings

We all want to save money, and technology is the best way to cut costs when it comes to dealing with large amounts of data. Digitizing the remediation process, your organization can significantly slash costs. For example, Ondato’s KYC solution can reduce KYC costs by more than a half, with a single verification costing less than €1 or even lower, depending on the number of verifications you need to perform. Multiply that across tens of thousands of customers, and the savings are enormous. Not to forget that a human analyst can handle only a few customer updates per hour, whereas a well-configured KYC engine can process 50 or more customers in the same time. In short, tech allows you to “do more with less”, which is crucial given budget and staffing constraints.

Automated Data Collection and Verification

Repetitive, manual tasks kill productivity. Software can instantly flag issues like expired IDs and guide customers through digital portals and apps to update information – instead of emailing customers one by one and tracking responses in a spreadsheet. AI-driven systems verify identity documents in under 30 seconds, a task that takes humans 10–20 minutes, while performing instant sanctions and PEP screening. For example, digital solutions can provide an all-in-one compliance platform where customers can securely submit documents, and the system will automatically verify their identity documents, using AI for facial recognition, hologram checks on IDs, and so on, and check against sanctions and PEP lists in seconds.

Improved Data Accuracy and Fraud Detection

Accurate data is the key to fraud prevention. KYC platforms with AI and machine learning analyze document uploads for signs of forgery or tampering. For example, whether or not a submitted ID photo was photoshopped. They also do biometric checks, such as liveness detection and face matching, to verify genuine customers, to make sure the customer is genuine, and not imposter. And the accuracy rates can be as high as 99%+. All of this not only enhances the remediation but also creates a more resilient system against future fraud and compliance issues.

Centralized Case Management

Modern platforms track every remediation action in one dashboard, showing case status at a glance –every customer remediation case logged, assigned, and monitored. For example, you can see which cases are pending customer response, which are under review, and which are completed. Meanwhile, automated audit trails log all communications and changes, making it easy to demonstrate compliance to regulators. So, if a regulator asks for proof that you updated Steven Wright’s KYC information, a case management system can pull up the entire history: initial data, request sent, new data received on X date, verified by analyst Y, etc.

How to Balance Customer Experience and Compliance

Yes, achieving compliance is very important, but it shouldn’t come at the expense of your customers’ trust or convenience. To properly balance customer experience and compliance obligations, you need to, first and foremost, communicate clearly and transparently to your customers why they need to update their information as part of KYC. Make sure they understand it’s not an arbitrary request – these updates keep their accounts secure and meet regulatory requirements.

Here are other things you should keep in mind:

Minimize friction in the update process. Use digital channels and user-friendly tools that let customers verify or submit documents quickly. Your goal is to make compliance updates feel as seamless as a routine online transaction.

Always provide clear instructions and support. Tell your customers exactly what information or documents are required and how to submit them, and offer help through multiple channels (like in-app chat, email or phone) so they feel guided and not lost.

Respect privacy and avoid redundant requests. Don’t ask for data you already have or information that isn’t absolutely necessary. Reassure customers that their personal details are protected and will only be used for compliance purposes.

Be thoughtful about timing and frequency. Reach out for KYC updates at sensible intervals, i.e. not so often that it frustrates customers, but regularly enough to stay compliant. Avoid contacting customers at inconvenient times, and consider issuing update requests with natural account milestones or periodic reviews.

But above all, show empathy and appreciation. Acknowledge that these checks can be an inconvenience and thank customers for their cooperation. Let them know you value their time and their partnership in keeping the financial system safe.

Conclusion

Continuous compliance is the new normal, and KYC remediation is a core component of that journey, as well as an ongoing commitment. As regulations tighten and financial crimes evolve, organizations must put even more effort in keeping customer data accurate and complete. That’s why KYC remediation, the systematic review and update of customer records, is essential in avoiding fines, preventing crime, and maintaining trust. While the process can be challenging due to data volume, manual work, and customer concerns, proven strategies like risk-based prioritization and automation make it manageable.

And technology can seriously help financial institutions to optimize the KYC remediation process. Yet, it’s important to note that technology doesn’t eliminate the need for human judgment – rather, it frees up your employees to focus on the nuanced decisions (like investigating truly suspicious cases or handling VIP customers sensitively) while the system handles the grunt work.

FAQ